Published on Thursday, July 25, 2024

US | Are higher risk premia preventing long-term yields from falling further?

Summary

The futures market is almost fully pricing in that the Fed will cut rates by 50 bps this year (95% implied chances) and continue to anticipate roughly 100 bps worth of rate cuts next year. Markets are certain of a rate cut in September, but are also likely pricing in risks in the event of a Trump’s second term.

Key points

- Key points:

- Growing expectations that the Fed is about to begin a rate-cut cycle (in September) have not fully reflected along the entire yield curve.

- The 2-year yield has declined by 30 bps since late June on strong investors’ demand at the most recent auctions; buyers are likely seeking to lock in higher rates before cuts from the Fed.

- The 10-year yield has been hovering in a narrow range around 4.3%, only breached temporarily in the early days of July to a 4.5% high following the first presidential debate.

- Markets probably brought out their perception of greater long-term risks in the event of a Trump’s second term, since he would likely favor more inflationary trade and tax policies.

- The FOMC is unlikely to say that recent “good data” is enough to consider rate cuts, but a further recognition of risks around their employment goal could drive the 10y-2y yield spread above zero soon.

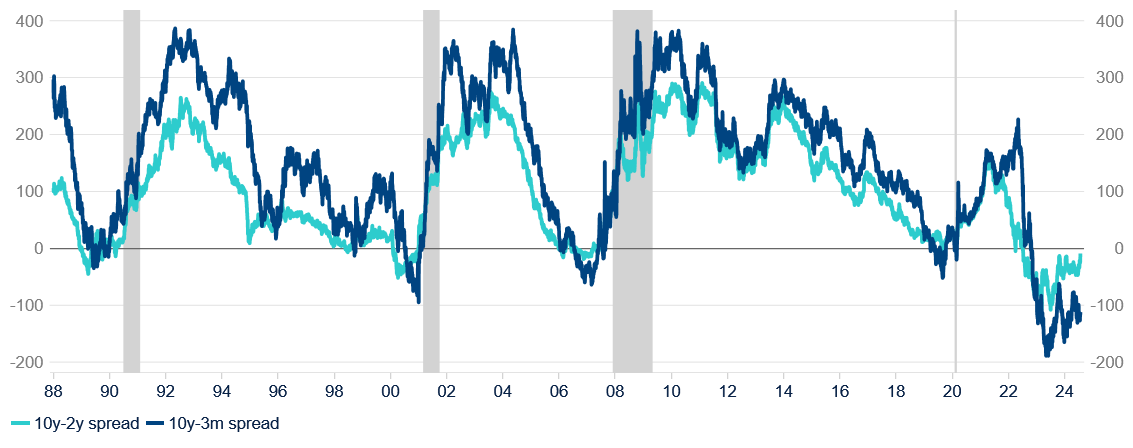

TREASURY YIELD SPREADS

(BPS)

The gray shaded areas indicate US recessions as defined by NBER. Source: BBVA Research / NBER / Treasury

Geographies

- Geography Tags

- Global

Topics

- Topic Tags

- Central Banks

- Financial Markets

Documents and files

Authors

Was this information useful?